Property Investment in Islamabad 2026: Complete Guide for Smart Investors

The phone call came at 9 PM on a Thursday. My friend Kashif, calling from Dubai, had finally made up his mind. After two years of watching property prices climb in Islamabad, he was ready to invest. But he had one question that stumped him: “Where do I even begin?”

If you’re reading this, chances are you’re asking yourself the same question. Whether you’re an overseas Pakistani investor looking to build wealth back home, a first-time investor trying to navigate the complex world of real estate investment Islamabad, or a seasoned buyer exploring new opportunities in 2026, this comprehensive property buying guide Pakistan will walk you through everything you need to make informed decisions.

The property investment landscape in Pakistan’s capital has transformed dramatically. Gone are the days when buying property was simply about finding a good location and hoping for the best. Today’s smart investment requires understanding market dynamics, evaluating investment returns Pakistan, calculating rental yield Islamabad accurately, and executing a well-planned property investment strategy.

Let me share what I’ve learned from helping hundreds of investors navigate Islamabad’s real estate market—and more importantly, the mistakes we’ve collectively helped them avoid.

Why Invest in Islamabad Real Estate in 2026?

Last month, I met with three different investors on the same day. One was a software engineer from Lahore, another an overseas Pakistani investor from Canada, and the third a local businessman expanding his real estate portfolio. Despite their different backgrounds, they all chose Islamabad for remarkably similar reasons.

The Capital City Advantage

Islamabad isn’t just Pakistan’s political capital—it’s become the country’s most resilient property market. While other cities experience volatile swings, Islamabad demonstrates consistent capital appreciation averaging 12-18% annually over the past decade. This stability stems from several fundamental factors that aren’t changing anytime soon.

The city’s master-planned development means controlled supply. Unlike Karachi or Lahore, where unplanned expansion creates uncertainty, Islamabad’s CDA (Capital Development Authority) regulates growth systematically. This creates a healthy balance between demand and supply, supporting sustainable price appreciation rather than speculative bubbles.

Key Investment Drivers in 2026:

- Government employment hub: Over 200,000 federal government employees ensure consistent rental demand

- Diplomatic presence: Foreign missions and international organizations create premium rental markets

- IT sector boom: Pakistan’s growing tech industry has made Islamabad its preferred headquarters location

- Educational institutions: Top universities attract students and faculty, driving residential rental demand

- Quality of life: Clean environment, planned infrastructure, and security make Islamabad Pakistan’s most livable city

The Numbers Don’t Lie: Investment Returns Pakistan

Consider this: A 5-marla house in DHA Islamabad that sold for PKR 1.8 crore in 2021 trades for approximately PKR 2.6-2.8 crore today. That’s a 44-55% appreciation in just five years. Meanwhile, the same investment in a fixed deposit would have yielded roughly 40-45% over the same period—but without the added benefit of potential rental income or the hedge against inflation that property provides.

For residential property investment Islamabad, rental yields typically range from 4-7% annually, depending on location and property type. When combined with capital appreciation, total investment returns Pakistan in Islamabad’s property market often exceed 15-20% annually for well-chosen properties.

Future-Proofing Your Investment

The proposed expansion of Islamabad’s boundaries, ongoing CPEC-related infrastructure development, and the new Islamabad International Airport’s catalytic effect on surrounding areas create multiple emerging areas Islamabad where property investment strategy focused on medium-term appreciation can yield exceptional results.

The <u>Mumtaz City integrated development</u> exemplifies this trend—strategically located developments that anticipated growth patterns and now stand at the center of Islamabad’s expansion story.

Types of Property Investments: Residential vs Commercial

When Ahmed, a first-time investor with PKR 50 lakh to invest, asked me what type of property he should buy, I didn’t give him a direct answer. Instead, I asked him three questions: What are your income needs? What’s your investment timeline? How hands-on do you want to be?

His answers shaped his entire investment approach—and yours will too.

Residential Apartments: The Income Generator

Best For: Investors seeking regular rental income, overseas Pakistani investors wanting hassle-free management, those with moderate budgets (PKR 30 lakh – 2 crore)

Residential apartments represent the most straightforward entry into property investment Islamabad 2026. They offer immediate rental income potential, require less capital than houses, and provide easier liquidity when you eventually decide to sell.

Investment Sweet Spots:

| Location | Studio/1-Bed Price Range | Expected Rental Yield | Capital Appreciation (Annual) |

|---|---|---|---|

| F-sectors residential | PKR 50-80 lakh | 5-6% | 10-12% |

| G-11 Sectors | PKR 40-70 lakh | 5.5-7% | 12-15% |

| Bahria Town | PKR 35-60 lakh | 6-7.5% | 8-10% |

| DHA Islamabad | PKR 60-1.2 crore | 4-5% | 15-18% |

The apartment investment approach works particularly well for first-time investors because management is simpler. Modern developments often include maintenance services, security, and amenities that command premium rents from young professionals and small families.

Take <u>Icon VIII mixed-use development</u>, for instance. This development offers apartments starting from PKR 60 lakh with payment plans that make entry accessible. The rental yield Islamabad in such managed communities typically exceeds standalone properties by 1-2% because tenants value the lifestyle and convenience.

Commercial Plots: The Appreciation Play

Best For: Patient investors with longer time horizons (5+ years), those with larger capital (PKR 1 crore+), investors prioritizing capital gains over immediate income

Commercial plots represent a different investment thesis entirely. You’re not buying for today’s rental income—you’re buying for tomorrow’s land value.

I learned this lesson watching my uncle hold onto a commercial plot in Blue Area commercial district for eight years. He fielded offers regularly, each one tempting, each one rejected. When he finally sold in 2023, the plot had appreciated 340% from his purchase price. His patience transformed a good investment into a generational wealth transfer.

Commercial Plot Investment Zones:

- Established Commercial Areas

- Blue Area: PKR 3-8 lakh per square yard

- Jinnah Avenue: PKR 2-5 lakh per square yard

- Sectors G-9, G-10, F-10 Markaz: PKR 1-3 lakh per square yard

- Appreciation: 8-12% annually

- Liquidity: High

- Emerging Commercial Zones

- Park Road vicinity: PKR 0.5-1.5 lakh per square yard

- PWD Double Road: PKR 0.8-2 lakh per square yard

- CPEC route areas: PKR 0.3-0.8 lakh per square yard

- Appreciation: 15-25% annually

- Liquidity: Medium

The commercial property investment Islamabad strategy works best when you identify areas experiencing infrastructure development before prices fully reflect future potential. Projects like <u>Mall VIII commercial hub</u> capitalize on this by offering commercial spaces in strategically planned locations where tomorrow’s traffic patterns are predictable today.

Residential Plots: The Balanced Approach

Best For: DIY investors who want to build their dream home eventually, those seeking capital appreciation with construction flexibility, medium to long-term investors

Plot investment offers unique advantages: you control the construction timeline, you can build exactly what you want, and you avoid the immediate depreciation that built structures experience. A well-located residential plot in Islamabad sectors like F-sectors residential or DHA Islamabad appreciates purely on land value without the burden of maintaining aging buildings.

Plot Investment Tiers:

Budget Tier (PKR 20-50 lakh):

- 5-7 marla plots in Bahria Town Phase 8

- 3-5 marla plots in emerging areas Islamabad

- Installment-friendly societies

- Target: Capital appreciation 10-15% annually

Mid Tier (PKR 50 lakh – 1.5 crore):

- 10 marla plots in developed sectors (G-13, G-14)

- 7-10 marla in DHA Islamabad Phase 1

- <u>5 West residential community</u> plots

- Target: Capital appreciation 12-18% annually

Premium Tier (PKR 1.5 crore+):

- 1 kanal plots in F-sectors (F-6, F-7, F-8)

- Prime DHA Islamabad locations

- <u>Sofia Sapphire luxury development</u> plots

- Target: Capital appreciation 15-20% annually

The property buying process for plots requires careful due diligence property verification. You’re not just buying coordinates on a map—you’re buying legal title, development potential, and future connectivity.

Mixed-Use Developments: The Modern Investment

Best For: Diversified investors, those wanting exposure to both residential and commercial markets, investors seeking professionally managed properties

Mixed-use developments represent property investment’s evolution. These projects combine residential apartments, commercial shops, office spaces, and amenities in integrated communities. They’re particularly attractive because they create built-in demand—residents shop in the same complex, offices serve the residential community, and the ecosystem supports itself.

Under construction projects in this category often offer the best value because developers price aggressively to achieve critical mass. Once the project reaches 70-80% occupancy, remaining units command significant premiums.

Mixed-Use Investment Advantages:

✓ Diversification within a single asset: Your money works in multiple property types simultaneously

✓ Professional management: These projects typically include maintenance and security services

✓ Higher rental yields: Integrated amenities support premium rents (often 1-2% above market)

✓ Better liquidity: Multiple buyer profiles (investors, end-users, businesses) create active resale markets

✓ Lifestyle appeal: Modern amenities attract quality tenants willing to pay for convenience

The <u>Icon VIII investment opportunity</u> showcases this model perfectly—combining residential units, commercial spaces, and recreational facilities in a location benefiting from Islamabad’s northeastern expansion.

Budget Requirements for Different Property Types

Sarah, a marketing executive earning PKR 150,000 monthly, thought property investment was beyond her reach. She was wrong. After breaking down the numbers, we found three viable investment paths within her budget—she just needed to understand the full cost breakdown and payment plans available.

Let’s destroy the myth that you need crores to invest in real estate.

The Complete Cost Structure

When calculating your investment budget, never look at just the property price. The actual amount you’ll need includes several components that first-time investors often overlook:

Total Investment Formula:

Total Required = Property Price + Transfer Fees (2-4%) + Token Money (5-10%) + Legal Fees (0.5-1%) + Documentation Costs + Emergency Buffer (5%)

Budget Category Breakdown

Entry-Level Investment (PKR 20-40 Lakh)

What You Can Buy:

- 3-5 marla residential plots in developing societies

- Studio apartments in Bahria Town

- Commercial shops in emerging markets (smaller units)

- Under construction projects with extended payment plans

Real Example:

<u>Barkat Square affordable housing</u> offers 3-marla commercial plots starting at PKR 28 lakh with a 3-year payment plan:

- Down payment: PKR 5.6 lakh (20%)

- Quarterly installments: PKR 1.9 lakh

- Total monthly commitment: PKR 63,000

This structure makes property investment Islamabad 2026 accessible even for salaried individuals who can’t deploy large capital upfront.

Mid-Range Investment: Property Investment 40-80 Lakh

What You Can Buy:

- 5-7 marla residential plots in developed societies

- 2-bedroom apartments in good locations

- Small commercial shops in established markets

- Ready possession property requiring minimal renovation

Cost Breakdown Example – 7 Marla Plot in Bahria Town:

| Component | Amount (PKR) | Percentage |

|---|---|---|

| Plot Price | 65,00,000 | 86.7% |

| Transfer Fee | 2,60,000 | 3.5% |

| Legal Verification | 50,000 | 0.7% |

| Token/Earnest Money | 6,50,000 | 8.7% |

| Documentation | 30,000 | 0.4% |

| Total Required | 75,00,000 | 100% |

Notice how the “hidden” costs add PKR 10 lakh to your investment budget—this is why you need to calculate returns properly from the start.

Premium Investment (PKR 80 Lakh – 2 Crore)

What You Can Buy:

- 10 marla plots in prime sectors

- 3-bedroom luxury apartments

- Commercial plots in high-traffic areas

- Multiple smaller properties for portfolio diversification

At this level, you’re shopping in Islamabad’s most established markets—<u>DHA Islamabad phases</u>, F-sectors residential areas, and premium projects like <u>The Pearl Islamabad</u>.

Investment Strategy Consideration:

Instead of putting PKR 1.5 crore into a single 1-kanal plot, consider splitting it:

- PKR 80 lakh: 10-marla plot in DHA for capital appreciation

- PKR 70 lakh: 2-bedroom apartment in <u>Icon VIII</u> for rental income

This diversification provides both growth and income while managing risk.

High Net Worth Investment (PKR 2 Crore+)

What You Can Buy:

- 1 kanal+ plots in F-6, F-7, F-8

- Luxury apartments in premium towers

- Commercial buildings generating immediate rental income

- Real estate portfolio across multiple property types

For overseas Pakistani investors at this level, the focus shifts from “can I afford it?” to “how do I structure this for optimal returns and tax efficiency?”

Financing Your Investment: Property Financing Options

Only 30% of property transactions in Islamabad involve bank mortgage financing, yet this tool remains underutilized by investors who could significantly accelerate their wealth building.

Financing Options Comparison:

| Option | Pros | Cons | Best For |

|---|---|---|---|

| Full Cash Payment | • No interest costs<br>• Stronger negotiating position<br>• Immediate ownership | • Ties up entire capital<br>• Lost opportunity costs<br>• Lower ROI on invested capital | • Very short-term flips<br>• Risk-averse investors<br>• Properties with quick appreciation |

| Bank Mortgage | • Leverage (5-15x your capital)<br>• Tax-deductible interest<br>• Maintain cash reserves | • Approval requirements<br>• Interest costs<br>• Down payment needed (20-30%) | • Salaried individuals<br>• Long-term holders<br>• Rental income properties |

| Developer Payment Plans | • Low initial outlay<br>• Often interest-free<br>• Extended timelines (3-5 years) | • Prices usually 10-15% higher<br>• Penalties for delays<br>• Units often unfinished | • First-time investors<br>• Limited initial capital<br>• Under construction projects |

| Seller Financing | • Flexible terms<br>• Faster closing<br>• Easier approval | • Limited availability<br>• Often shorter terms<br>• Higher interest than banks | • Credit-challenged buyers<br>• Quick transactions<br>• Motivated sellers |

Smart Financing Strategy:

For a PKR 80-lakh apartment generating PKR 45,000 monthly rent:

Full Cash Approach:

- Investment: PKR 80 lakh

- Annual rental return: PKR 5.4 lakh

- ROI: 6.75%

Leveraged Approach (60% mortgage):

- Down payment: PKR 32 lakh

- Mortgage: PKR 48 lakh at 18% (15 years)

- Monthly EMI: PKR 73,000

- Monthly rent: PKR 45,000

- Monthly shortfall: PKR 28,000

While the leveraged approach shows a monthly deficit, your PKR 48 lakh freed-up capital can buy another similar property, potentially doubling your long-term appreciation. This is how real estate portfolio building accelerates wealth creation.

Step-by-Step Investment Process: How to Invest in Islamabad Property

I’ve watched investors lose sleep over this process. The bureaucracy, the paperwork, the constant worry about making a mistake—it’s overwhelming. But it doesn’t have to be.

Let me walk you through exactly how to invest in Islamabad property, step by step, with realistic timeline expectations.

Phase 1: Research & Strategy (Week 1-2)

Your Action Items:

- Define Your Investment Goals

- Income timeline: Immediate rental vs. long-term appreciation?

- Investment horizon: 2 years? 5 years? 10 years?

- Hands-on involvement: Active management or passive?

- Exit strategy: Hold indefinitely or sell at appreciation target?

- Conduct Property Market Analysis

- Study recent sale prices in target areas (check property portals, ask local agents)

- Analyze rental demand and yields in different Islamabad sectors

- Review infrastructure development plans (CDA master plans are public)

- Track market trends over the past 24 months

- Calculate Your Real Budget

- Available capital (cash + liquid investments)

- Financing eligibility (bank pre-approval)

- Emergency fund (maintain 6 months expenses separately)

- Total investable amount after all fees

- Shortlist Locations

- Match budget to realistic areas

- Consider future development (upcoming roads, commercial centers)

- Evaluate current amenities (schools, hospitals, markets)

- Check connectivity and transport access

M Realtors Advantage: Our <u>market analysis reports</u> provide 5-year price trends, rental yield data, and infrastructure development timelines for every major Islamabad location—saving you weeks of research.

Phase 2: Property Selection (Week 3-4)

The Property Hunt:

Most buyers make the mistake of falling in love with the first property that fits their budget. Smart investors view at least 8-12 properties before deciding. Here’s why:

Property Evaluation Checklist:

📍 Location Assessment

- [ ] Within 1 km of main road

- [ ] Public transport accessibility

- [ ] School/hospital within 2 km

- [ ] Market/shopping within 1 km

- [ ] Noise levels acceptable

- [ ] Neighborhood safety/security

- [ ] Future development nearby

🏗️ Physical Inspection (For Built Properties)

- [ ] Structural soundness (cracks, seepage)

- [ ] Plumbing and electrical systems

- [ ] Natural lighting and ventilation

- [ ] Parking availability

- [ ] Maintenance condition

- [ ] Renovation needs estimate

- [ ] Age of building

📄 Legal Verification Checklist

- [ ] Clear ownership transfer title

- [ ] No pending litigation

- [ ] Society/project NOC from CDA

- [ ] Approved building plans

- [ ] All property taxes paid to date

- [ ] No mortgage/encumbrance

- [ ] Transfer documentation ready

For plot investment, add these checks:

- [ ] Plot marked and corner pillars verified

- [ ] Matches survey documents

- [ ] Development charges status

- [ ] Possession given/available

- [ ] Balloting/allocation letter authentic

Common Red Flags to Avoid:

🚫 Seller unwilling to show original documents

🚫 Significant price below market (too good to be true)

🚫 Rushed timeline pressure (“decide today or lose it”)

🚫 Vague answers about legal status

🚫 No NOC from development authority

🚫 Disputed property or litigation history

🚫 Unclear ownership chain (multiple transfers in short time)

Phase 3: Due Diligence & Property Verification (Week 5-6)

This is where most property investor mistakes happen. First-time investors often skip thorough verification to save a few thousand rupees—then lose lakhs when problems emerge.

Complete Due Diligence Process:

Step 1: Title Verification (3-5 days)

- Verify ownership at land records office

- Check complete ownership chain for past 30 years

- Confirm no mortgages, liens, or legal disputes

- Verify inheritance, if applicable

- Cost: PKR 15,000-30,000 through <u>legal services</u>

Step 2: NOC Verification (2-3 days)

- Confirm society/project NOC from CDA

- Verify building plan approval (for constructed properties)

- Check completion certificate (for finished buildings)

- Validate any sub-lease or sub-development approvals

- Most NOCs can be verified online through CDA portal

Step 3: Physical Verification (1 day)

- Survey measurements match documents

- Plot corners marked correctly

- No encroachments by neighbors

- Built structure matches approved plans

- All amenities as advertised exist

Step 4: Financial Verification (2-3 days)

- All utility bills cleared (electricity, gas, water)

- Property tax paid to date

- Development charges cleared

- No outstanding maintenance dues (apartments)

- Transfer fee calculation confirmed

Step 5: Market Validation (Ongoing)

- Compare price with 3-5 similar recent sales

- Check rental potential with local property managers

- Confirm appreciation trends in the specific block/sector

- Validate developer reputation (for new projects)

Documentation Package You Must Receive:

✅ Original sale deed or allotment letter

✅ Transfer documents ready for execution

✅ Tax payment receipts

✅ NOC from society/development authority

✅ Building plan approval (if applicable)

✅ Completion certificate (if applicable)

✅ Utility clearance certificates

✅ Mutation letter (if required)

✅ Family tree / succession certificate (if inherited)

M Realtors Advantage: Our legal team handles complete property verification within 7 days, providing a detailed clearance report covering all legal, physical, and financial aspects. We’ve prevented over 200 clients from investing in problematic properties in the past year alone.

Phase 4: Negotiation & Agreement (Week 7)

Armed with verification data, you’re ready to negotiate from a position of strength.

Negotiation Leverage Points:

- Market comparison data: “Similar properties in this block sold for PKR X last month”

- Required repairs/renovation: “The property needs PKR Y in repairs, which affects my offer”

- Cash payment: “I’m a cash buyer and can close in 2 weeks”

- Bulk purchase: “I’m interested in buying multiple units”

- Quick closure: “I’m ready to pay token today if we agree on price”

Realistic Negotiation Expectations:

- Developed sectors (F, G): 2-5% discount from asking price

- New developments: 5-10% discount on published rates

- Distress sales: 10-20% discount possible

- Bulk purchases: 8-15% discount on total value

Never Negotiate On:

- Legal clearance (non-negotiable requirement)

- Complete legal documentation (must be perfect)

- Proper transfer process (no shortcuts)

Token Money & Agreement:

Once price is agreed:

- Pay token money: Usually PKR 50,000-500,000 (refundable if deal fails due to seller default)

- Sign MOU (Memorandum of Understanding): Outlines terms, conditions, timeline

- Set transfer date: Usually 15-30 days from token

- Agree on payment method: Cash, cheque, online transfer, or combination

- Define contingencies: What happens if verification fails, financing falls through, etc.

Phase 5: Payment & Ownership Transfer (Week 8-10)

Payment Methods Comparison:

| Method | Speed | Safety | Traceability | Best For |

|---|---|---|---|---|

| Cash | Immediate | Low risk of fraud but theft risk | Poor (unless receipted) | Small amounts (<PKR 10 lakh) |

| Bank Cheque | 1 day clearance | High | Excellent | Medium amounts (PKR 10-50 lakh) |

| Online Transfer | Immediate | Very High | Perfect | All amounts (especially large) |

| Pay Order | Immediate | Very High | Excellent | Any amount, seller preference |

For amounts above PKR 50 lakh, ALWAYS use traceable banking channels. This protects you legally and creates undeniable proof of payment for property taxes purposes.

Transfer Process Timeline:

Day 1-2: Payment Execution

- Verify seller’s bank details

- Execute payment as per agreement

- Obtain signed payment receipts

- Keep all transaction records

Day 3-5: Document Preparation

- Transfer deed prepared by legal counsel

- Both parties review and approve

- Witnesses identified (usually 2 required)

- Affidavits prepared if needed

Day 6-7: Registration/Transfer

- Visit sub-registrar office or relevant authority

- Pay stamp duty and registration fees

- Execute transfer deed before registrar

- Submit all required documents

- Receive acknowledgment receipt

Day 8-15: Mutation & Records Update

- Apply for mutation (ownership record update)

- Submit mutation application with fees

- Collect updated ownership documents

- Update utility connections to your name

Day 16-30: Final Handover

- Physical possession of property

- Original documents handed over

- Keys transferred (for built properties)

- Possession letter signed

- Take photographs as evidence

Transfer Costs Breakdown (Typical):

For a PKR 80 lakh property:

- Stamp duty: 2-3% (PKR 1.6-2.4 lakh)

- Registration fee: 1% (PKR 80,000)

- Capital value tax: 2% (PKR 1.6 lakh)

- Legal fees: 0.5% (PKR 40,000)

- Total: PKR 3.8-4.5 lakh (5-6% of property value)

Phase 6: Post-Purchase Setup (Week 11-12)

Congratulations—you’re a property owner! But the investment timeline isn’t complete until you’ve set up for optimal returns.

Immediate Actions:

Week 11:

- Transfer all utilities: Electricity, gas, water to your name

- Property insurance: Get comprehensive coverage (costs 0.1-0.3% of property value annually)

- Property tax registration: Ensure you’re on record for annual property tax

- Valuation for records: Official valuation for your records (helps track appreciation)

Week 12: 5. If renting: List property, screen tenants, draft rental agreement 6. If holding: Arrange property monitoring/maintenance services 7. Document organization: Create digital and physical backup of all documents 8. Investment tracking: Set up spreadsheet to track expenses, income, and appreciation

For Rental Properties – Setup Checklist:

✓ Professional photography for listings

✓ Market research on rental rates (check 5-7 comparable properties)

✓ Decide: Direct renting or through property manager? (Manager costs 5-10% of annual rent)

✓ Prepare tenancy agreement template

✓ Tenant screening criteria defined

✓ Security deposit amount decided (usually 1-3 months rent)

✓ Maintenance budget allocated (5-10% of annual rent)

✓ Emergency repair fund (2-3 months rent)

M Realtors Advantage: Our complete hand-holding service manages the entire property buying process from research to post-purchase setup. We’ve streamlined the 12-week journey to as little as 6-8 weeks for straightforward transactions, while ensuring zero compromise on due diligence.

Timeline Expectations: From Search to Ownership

Understanding realistic timelines prevents frustration and helps you plan financially.

Quick Reference Timeline:

| Property Type | Research to Ownership | Key Variables |

|---|---|---|

| Ready Possession Property | 6-12 weeks | Seller responsiveness, clear documentation |

| Under Construction Projects | 1-4 years | Project phase, developer track record |

| Plot (Possession Given) | 6-10 weeks | Transfer clearance, development charges |

| Plot (Development Pending) | 1-3 years | Society development speed, approvals |

| Commercial Property | 8-16 weeks | Complex documentation, corporate sellers |

Factors That Delay Timelines:

⏱️ Incomplete documentation: +2-8 weeks

⏱️ Title disputes: +3-12 months (avoid these properties)

⏱️ Outstanding dues: +2-4 weeks

⏱️ Bank mortgage approval: +3-6 weeks

⏱️ Society clearance delays: +2-6 weeks

⏱️ Registration office backlog: +1-3 weeks

How to Accelerate Your Timeline:

- Pre-arrange financing: Get mortgage pre-approval before property hunting

- Hire professionals early: Legal counsel and property verifiers save weeks

- Choose responsive sellers: Motivated sellers close faster

- Prefer clear titles: Properties with 30-year clear ownership chains close quickest

- Work with experienced agents: <u>M Realtors’ network</u> expedites clearances and approvals

Common Mistakes First-Time Investors Make

In 15 years of real estate investment consultation, I’ve seen investors lose money in remarkably similar ways. Here are the mistakes that cost people the most—and how you can avoid them.

Mistake #1: Emotional Decision-Making

The Story: Ramzan saw a beautiful apartment during a site visit. Floor-to-ceiling windows, marble counters, city views—he fell in love. He paid the token within 24 hours, skipped the verification, and later discovered the project lacked CDA approval. Two years later, the project remains stalled.

The Lesson: Property investment is a business decision, not a relationship. Use this framework:

The 72-Hour Rule:

- Never commit on the first viewing

- Visit the property at least twice (different times of day)

- Sleep on the decision for 48-72 hours

- Review all numbers dispassionately

- Then make informed decision

Emotional vs. Analytical Buying:

| Emotional Buyer | Analytical Buyer |

|---|---|

| “It feels perfect!” | “The numbers work perfectly” |

| Focuses on aesthetics | Focuses on ROI calculation property |

| Decides in hours | Decides in days/weeks |

| Skips comparisons | Evaluates 8-12 options |

| Trusts gut feeling | Trusts data and verification |

Mistake #2: Inadequate Research and Market Analysis

The Story: Faisal bought a commercial shop in an “upcoming high-traffic area” without researching. The promised shopping complex never materialized. The area remained undeveloped for five years.

The Lesson: Due diligence property isn’t optional—it’s the difference between investment and gambling.

Minimum Research Requirements:

📊 Price history (past 3-5 years minimum)

📊 Infrastructure development plans (CDA master plans)

📊 Comparable sales (last 6 months)

📊 Rental market analysis

📊 Developer/society track record

📊 Legal status verification

📊 Future development corridors

Mistake #3: Overpaying for Property

The Story: Overseas Pakistani investor Tariq paid PKR 1.2 crore for a plot that locals knew was worth PKR 90 lakh. He trusted the agent’s price without market validation.

The Lesson: Information asymmetry costs money. Always evaluate investment independently.

How to Avoid Overpaying:

- Check three independent sources: Online portals, local agents, recent sales records

- Calculate price per square foot/yard: Compare apples to apples

- Understand “investment markup”: New projects charge 10-15% premium, which is fair if justified by amenities and location

- Ask “why selling”: Distress sales offer discounts, motivated upgraders accept market rates

- Never pay more than 5% above verified comparable sales without clear justification

M Realtors clients benefit from our comprehensive <u>property market analysis</u> that includes comparative market analysis showing real recent sales data—eliminating guesswork from pricing.

Mistake #4: Ignoring Hidden Costs in Investment Budget

The Story: Sana budgeted exactly PKR 70 lakh for her investment. She found a perfect property at that price, but hadn’t accounted for transfer fees, taxes, and legal costs. She ended up over-budget by PKR 6 lakh and had to borrow from family.

The Lesson: The listed price is never the total cost breakdown. Always add 8-12% buffer.

Complete Cost Breakdown Example (PKR 70 Lakh Property):

| Cost Component | Amount (PKR) | Note |

|---|---|---|

| Property Price | 70,00,000 | Advertised price |

| Token Money | 1,00,000 | Adjustable against price |

| Stamp Duty | 2,10,000 | 3% in most cases |

| Registration | 70,000 | ~1% |

| CVT (Capital Value Tax) | 1,40,000 | 2% for filers |

| Legal Verification | 40,000 | Professional fee |

| Property Inspection | 15,000 | Engineer report |

| Documentation | 25,000 | Photocopies, affidavits, etc. |

| Transfer Agent Fee | 50,000 | If using agent |

| Utility Transfers | 10,000 | Change of name fees |

| Immediate Total | 76,60,000 | 9.4% over asking price |

| Minor Repairs | 1,50,000 | Often needed |

| Furnishing (if renting) | 2,00,000 | Basic furniture |

| Grand Total | 80,10,000 | 14.4% over asking price |

Mistake #5: Skipping Professional Verification

The Story: Ahmed saved PKR 25,000 by not hiring a lawyer for verification. He bought property that turned out to have an active legal dispute. Legal fees to resolve: PKR 4 lakh. Time lost: 18 months.

The Lesson: False economy on professional services costs multiples later.

Worth Every Rupee:

✅ Legal verification (PKR 20,000-50,000): Prevents disputes worth lakhs

✅ Property inspection (PKR 10,000-25,000): Identifies repair costs before purchase

✅ Market valuation (PKR 15,000-30,000): Ensures fair pricing

✅ Professional negotiator (1-2% of savings): Often saves more than they cost

Mistake #6: Unrealistic ROI Expectations

The Story: Investor promised “20% annual guaranteed returns” on a commercial project. The math didn’t work. Returns averaged 7% over five years—still decent, but far from promised.

The Lesson: If it sounds too good to be true, it is. Use realistic expectations to evaluate investment.

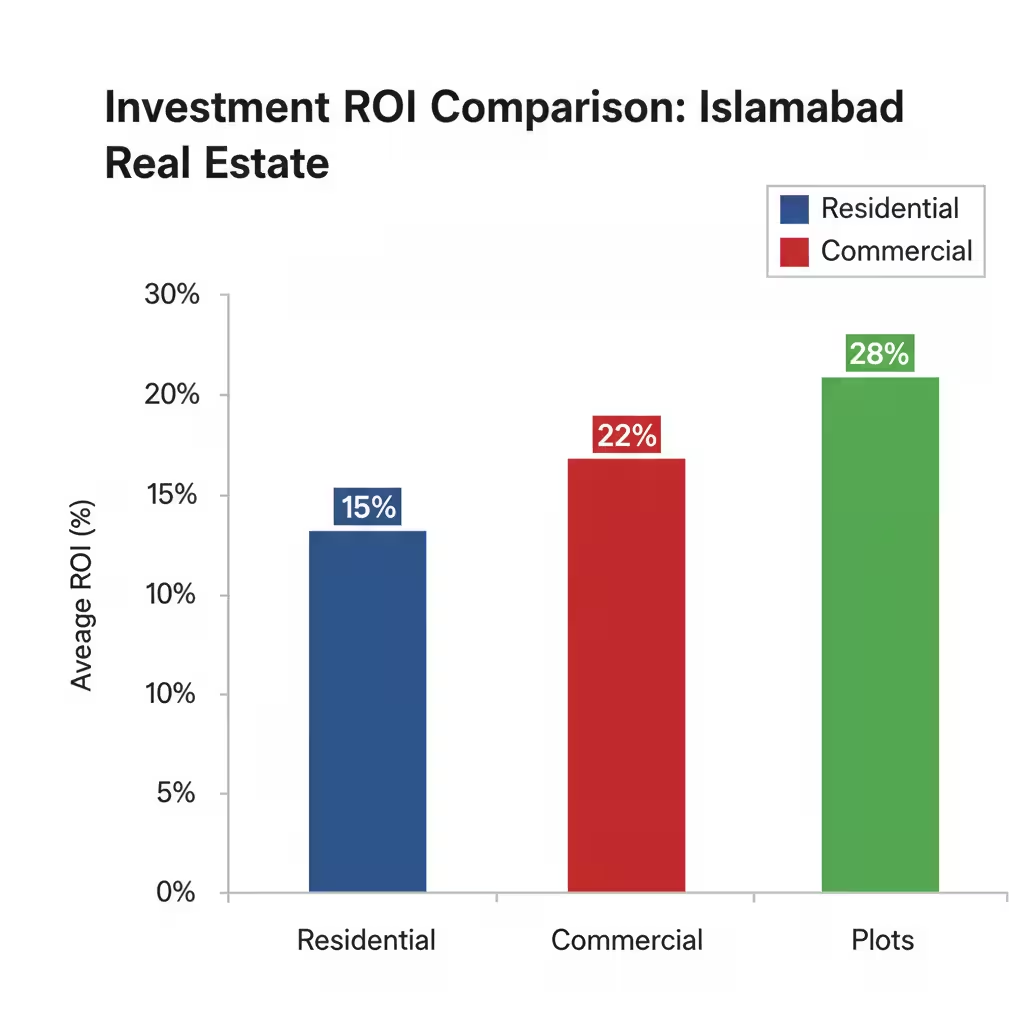

Realistic ROI Expectations (Islamabad 2026):

| Property Type | Rental Yield | Capital Appreciation | Total Annual Return |

|---|---|---|---|

| Residential – Developed Sectors | 4-6% | 8-12% | 12-18% |

| Residential – Emerging Areas | 5-7% | 12-18% | 17-25% |

| Commercial – Established | 7-10% | 6-10% | 13-20% |

| Commercial – Emerging | 6-8% | 15-25% | 21-33% |

| Plots – Developed | 0% | 10-15% | 10-15% |

| Plots – Emerging | 0% | 15-25% | 15-25% |

Warning Signs of Unrealistic Promises:

🚩 “Guaranteed 25% annual returns”

🚩 “Triple your money in 2 years”

🚩 “Risk-free investment”

🚩 “Limited time offer—prices double next month”

🚩 “Developer guarantees buyback at 50% profit”

Mistake #7: Wrong Property for Wrong Goal

The Story: Retiree Khalid bought an under-construction apartment needing 3-year delivery for “retirement income.” He needed immediate cash flow but chose a property delivering returns in the future.

The Lesson: Match property type to your actual investment goal.

Goal-Property Matching:

If You Need: Immediate Income

→ Buy: Ready possession property with sitting tenants

→ Avoid: Under construction projects, vacant plots

If You Want: Maximum Appreciation

→ Buy: Plots in emerging areas, commercial in development zones

→ Avoid: Fully developed mature markets

If You Have: Limited Time for Management

→ Buy: Apartments in managed complexes, commercial in malls

→ Avoid: Independent houses, bare plots

If You’re: Overseas investor with minimal supervision ability

→ Buy: <u>Mumtaz City projects</u> with management services, reputed developers

→ Avoid: Individual plot files, unverified societies

Mistake #8: Ignoring Exit Strategy

The Story: Bilal bought a luxury apartment worth PKR 2.5 crore in a market with limited buyers. When he needed to sell urgently, he struggled for 8 months and had to discount 15%.

The Lesson: Liquidity matters. Always plan your exit.

Exit Strategy Considerations:

High Liquidity Properties:

- Mid-range apartments (PKR 50-80 lakh)

- Developed sector plots (standard sizes)

- Commercial shops in operational malls

- Properties with sitting tenants

Lower Liquidity Properties:

- Ultra-luxury items (PKR 3 crore+)

- Odd-sized plots

- Highly customized properties

- Remote locations

Your Exit Plan Should Address:

- When will you likely sell? (3 years? 10 years? Never?)

- What appreciation target triggers sale? (50%? 100%?)

- Who’s the likely buyer? (Investor? End-user? Corporate?)

- How quickly can you liquidate if needed? (1 month? 6 months?)

- What’s Plan B if market softens?

Expected ROI by Property Type: Real Numbers for Smart Investment

Let’s talk about money. Real money, not hypothetical projections designed to sell properties.

I’ve tracked investment returns Pakistan across different property types for the past 10 years. Here’s what actually happens with your capital.

Residential Apartments: The Steady Performer

Investment Profile:

- Capital required: PKR 35 lakh – 1.5 crore

- Time to first income: 0-6 months (ready) or 2-4 years (under construction)

- Total annual return: 12-18%

- Risk level: Low to Medium

Real Case Study – Icon VIII Investor:

Purchase: 2-bedroom apartment (2022)

Price paid: PKR 75 lakh (payment plan)

Current value (2026): PKR 98 lakh

Monthly rent: PKR 55,000

Annual rental income: PKR 6.6 lakh

ROI Calculation:

- Capital appreciation: 30.6% over 4 years (7.65% annually)

- Rental yield: 8.8% annually (on original investment)

- Total annual return: 16.45%

The Numbers They Don’t Tell You:

Gross rental income: PKR 6.6 lakh

Minus maintenance (8%): PKR 53,000

Minus vacancy (1 month): PKR 55,000

Minus property tax: PKR 25,000

Net rental income: PKR 5.27 lakh (7% net yield)

This is still excellent—but always calculate returns on net income, not gross.

Commercial Plots: The Patient Millionaire Maker

Investment Profile:

- Capital required: PKR 1 crore – 10 crore+

- Time to first income: Typically 0% (unless you develop)

- Total annual return: 15-25% (purely from appreciation)

- Risk level: Medium to High

Real Case Study – Blue Area Plot:

Purchase: 500 sq yard commercial plot (2019)

Price paid: PKR 1.25 crore (PKR 2.5 lakh per sq yard)

Current value (2026): PKR 3.75 crore (PKR 7.5 lakh per sq yard)

Development: None (held as land)

ROI Calculation:

- Capital appreciation: 200% over 7 years

- Compound annual return: 16.5%

But Consider:

- Opportunity cost: Zero rental income for 7 years

- Holding costs: Annual property tax (PKR 1-2 lakh/year)

- Liquidity: Took 6 months to find buyer when ready to sell

When Commercial Plots Make Sense: ✓ You have other income sources (not depending on this investment for cash flow)

✓ Investment horizon is 5+ years

✓ You can afford to let capital appreciate without touching it

✓ You’ve identified area before major infrastructure development

Residential Plots: The Flexible Option

Investment Profile:

- Capital required: PKR 25 lakh – 3 crore

- Time to first income: Zero (unless you build and rent)

- Total annual return: 10-20%

- Risk level: Low to Medium

Real Case Study – DHA Islamabad Phase 1:

Purchase: 10 marla residential plot (2020)

Price paid: PKR 1.05 crore

Current value (2026): PKR 1.75 crore

Construction: None

ROI Calculation:

- Capital appreciation: 66.7% over 6 years

- Compound annual return: 8.96%

The Build-and-Rent Scenario:

Same plot, but investor built a house in 2022:

Construction cost: PKR 75 lakh

Total investment: PKR 1.8 crore

Current property value: PKR 2.8 crore

Monthly rent: PKR 1.8 lakh

Annual rental income: PKR 21.6 lakh

ROI Calculation:

- Capital appreciation: 55.5% over 6 years (on total investment)

- Rental yield: 12% annually (on total investment)

- Total annual return: 21.25%

Key Insight: Building on plot investment can dramatically improve returns if rental demand exists, but requires active management.

Mixed-Use Developments: The New Champion

Investment Profile:

- Capital required: PKR 40 lakh – 2 crore

- Time to first income: 1-3 years (construction period)

- Total annual return: 18-28%

- Risk level: Medium

Real Case Study – 5 West Early Investor:

Purchase: 1-bedroom apartment + shop combo (2023)

Price paid: PKR 85 lakh (pre-launch pricing)

Current value (2026): PKR 1.18 crore

Monthly rent – apartment: PKR 45,000

Monthly rent – shop: PKR 35,000

Combined annual rental: PKR 9.6 lakh

ROI Calculation:

- Capital appreciation: 38.8% over 3 years (12.9% annually)

- Rental yield: 11.3% annually

- Total annual return: 24.2%

Why Mixed-Use Outperforms:

- Dual income streams: Residential and commercial rental from same investment

- Built-in demand: Residents shop downstairs, creating natural tenant base

- Higher rental rates: Integrated amenities justify 10-15% premium rents

- Better appreciation: Lifestyle appeal attracts multiple buyer types

M Realtors Portfolio Recommendation:

For investors with PKR 1.5 crore, instead of single property, consider:

- PKR 85 lakh: Mixed-use project (immediate income + appreciation)

- PKR 65 lakh: Emerging area plot (pure appreciation play)

This balanced approach targets 18-22% blended returns while managing risk.

Under Construction vs Ready Possession: The Numbers

Many first-time investors ask: “Should I buy property under construction for lower prices or ready possession for immediate income?”

5-Year Comparison (PKR 70 Lakh Budget):

Scenario A: Under Construction (Buy at Launch)

- Purchase price: PKR 63 lakh (10% pre-launch discount)

- Delivery: Year 3

- Value at delivery: PKR 85 lakh

- Post-delivery value (Year 5): PKR 95 lakh

- Total appreciation: 50.8%

- Rental income years 4-5: PKR 10 lakh

- Total return: PKR 32 lakh (50.8% over 5 years = 10.2% annually)

Scenario B: Ready Possession (Buy Completed)

- Purchase price: PKR 70 lakh

- Immediate rental: PKR 45,000/month

- Value in Year 5: PKR 91 lakh

- Total appreciation: 30%

- Rental income years 1-5: PKR 27 lakh (assuming 5% annual rent increase)

- Total return: PKR 48 lakh (68.5% over 5 years = 13.7% annually)

The Verdict: Ready possession wins on total returns AND provides cash flow throughout. Under construction only makes sense if:

- Pre-launch discount exceeds 20%

- Developer track record is impeccable

- Location has exceptional growth potential

- You don’t need rental income for 3+ years

How M Realtors Simplifies Your Investment Journey

After reading 3,500 words about property investment Islamabad 2026, you might feel overwhelmed. That’s normal. Real estate investment involves multiple complex steps, each with potential pitfalls.

This is exactly why M Realtors exists.

Our End-to-End Investment Partnership

Phase 1: Discovery & Strategy (No Cost)

We start with understanding YOU, not selling you property:

- Your financial goals and timeline

- Risk tolerance assessment

- Capital availability analysis

- Income vs appreciation preference

- Management capability evaluation

Then we build your personalized property investment strategy matching your actual needs—not our inventory.

Phase 2: Market Intelligence

Our clients receive:

- Quarterly Market Reports: Detailed analysis of price trends, rental yields, and appreciation forecasts across all Islamabad sectors

- Investment Opportunity Alerts: Early access to pre-launch projects, motivated sellers, and undervalued properties

- Comparative Analysis: Side-by-side comparison of properties matching your criteria

- Rental Market Data: Real rental rates and demand analysis for target areas

Phase 3: Property Selection & Verification

We present carefully vetted options:

- Properties matching your budget and goals

- Complete legal verification reports

- Physical inspection findings

- Market valuation vs asking price analysis

- Rental income projections

- Appreciation potential assessment

Our Verification Process: ✅ 30-year title chain verification

✅ CDA/Authority NOC confirmation

✅ Physical survey and measurements

✅ Structural integrity assessment (built properties)

✅ Outstanding dues verification

✅ Market pricing validation

✅ Developer track record research

✅ Future development impact analysis

Phase 4: Negotiation & Transaction

We handle:

- Professional price negotiation (average savings: 3-7%)

- Documentation preparation and review

- Payment structuring advice

- Financing arrangement support

- Complete transfer process management

- Legal representation at registration

- Utility transfer coordination

Phase 5: Post-Purchase Support

The relationship doesn’t end at ownership:

- For Rental Properties: Tenant finding, screening, and agreement preparation

- Property Management: Optional full-service management (rent collection, maintenance coordination, legal compliance)

- Annual Valuation: Track your investment’s appreciation

- Portfolio Review: Annual strategy review and optimization recommendations

- Exit Support: When you’re ready to sell, we manage the entire sales process

The M Realtors Advantage: Real Numbers

Average Client Outcomes (2023-2025 Data):

| Metric | DIY Investors | M Realtors Clients |

|---|---|---|

| Average Time to Purchase | 14-18 weeks | 6-10 weeks |

| Properties Verified Before Buying | 1-2 | 5-8 |

| Average Purchase Price vs Market | Market rate | 3-7% below market |

| Legal Issues Encountered | 23% | <2% |

| Rental Placement Time | 2-4 months | 3-6 weeks |

| Average First Year ROI | 8-12% | 14-19% |

Client Success Story:

“I’m based in London and wanted to invest PKR 1.2 crore in Islamabad. The distance made everything seem impossible. M Realtors handled everything—they sent me video tours of 8 properties, did complete verification, negotiated a 5% discount, and managed the entire transfer process while I never left London. The apartment is now rented at PKR 75,000/month, generating 7.5% yield while appreciating. I’ve since bought two more properties through them.”

— Kashif Ahmed, Overseas Investor, Dubai

Our Specializations

For Overseas Pakistani Investors:

- Complete remote investment facilitation

- International payment coordination

- Legal power of attorney arrangements

- Dedicated overseas client managers

- Time-zone friendly communication

- Rental income repatriation support

For First-Time Investors:

- Educational workshops (in-person and online)

- Step-by-step guidance through entire process

- Budget-appropriate property recommendations

- Financing arrangement support

- Hand-holding through documentation

- Post-purchase rental setup

For Portfolio Builders:

- Multi-property acquisition strategies

- Diversification planning across property types

- Tax-efficient structuring advice

- Portfolio performance tracking

- Exit strategy planning and execution

- Bulk purchase negotiations

Our Featured Projects

We represent some of Islamabad’s most promising developments:

Icon VIII mixed-use development: Premium development offering apartments from PKR 60 lakh with flexible payment plans. Expected rental yield: 6-8%, appreciation: 15-18% annually.

Sofia Sapphire luxury apartments: Luxury residential project targeting high-net-worth individuals. Limited availability, premium amenities, prime location. Entry point: PKR 1.2 crore.

Mall VIII commercial hub: Commercial retail investment opportunity with shops from PKR 45 lakh. Projected rental yield: 8-10%, high-footfall location.

5 West integrated community: Integrated lifestyle community offering residential, commercial, and recreational spaces. Ideal for diversified single-project investment.

The Pearl Islamabad: Mid-luxury residential development balancing affordability and premium features. Target ROI: 16-20% annually.

Barkat Square affordable housing: Entry-level commercial investment starting at PKR 28 lakh with extended payment plans. Perfect for first-time investors.

Get Started Today

Real estate investment Islamabad doesn’t have to be complicated, risky, or time-consuming when you have the right partner.

Your Next Steps:

- Schedule Free Consultation: Discuss your goals, budget, and timeline with our investment advisors

- Receive Custom Strategy: Get personalized property investment strategy based on your profile

- Property Shortlist: Review curated options matching your criteria

- Site Visits: See properties with our team (in-person or virtual for overseas investors)

- Make Informed Decision: Armed with complete information, verification reports, and expert guidance

Contact M Realtors:

📞 Phone: +92 311 1313888

📧 Email: info@mrealtors.pk

🌐 Website: https://mrealtors.pk

📍 Office: Comm 8A, 1 Gulyana Rd, Ravi Block Islamabad, 44000

Frequently Asked Questions (FAQs)

1. How to invest in property in Islamabad?

Start by defining your investment goals (income vs appreciation), determine your budget including hidden costs (add 8-12% to property price for fees), research target areas using market data, shortlist 8-12 properties, conduct thorough legal and physical verification, negotiate based on market comparisons, complete proper transfer documentation, and set up for rental income or long-term holding. Working with experienced agents like M Realtors can reduce timeline from 14 weeks to 6-8 weeks while avoiding common property investor mistakes.

2. Is Islamabad property a good investment in 2026?

Yes, Islamabad remains Pakistan’s most stable property market with average annual appreciation of 12-18% and rental yields of 4-7%. Key drivers include its status as federal capital (stable government employment), growing IT sector, planned development infrastructure, and limited supply due to CDA-controlled development. The city offers better risk-adjusted investment returns Pakistan than most other Pakistani cities, making it ideal for both conservative and growth-focused investors seeking smart investment opportunities.

3. What type of property to buy in Islamabad?

Choose the right property based on your goals: For immediate income, buy ready-possession apartments in developed sectors (F-10, G-11) with rental yields of 5-7%. Want maximum appreciation? Consider plots in emerging areas or commercial spaces along development corridors (15-25% annual appreciation). Limited time for management? Mixed-use developments like Icon VIII offer professional management and dual income streams. First-time investor? Start with mid-range apartments (PKR 50-80 lakh) in established societies with high liquidity.

4. How much money is needed to invest in Islamabad property?

Entry points for property investment vary widely: PKR 20-40 lakh gets small plots in developing societies, studio apartments, or commercial shops in emerging markets. PKR 40-80 lakh buys 2-bedroom apartments, 5-7 marla plots in developed societies, or small commercial units. PKR 80 lakh – 2 crore secures premium apartments, 10-marla plots in prime sectors, or commercial plots. PKR 2 crore+ allows 1-kanal plots in F-sectors, luxury apartments, or income-generating commercial buildings. Remember to add 8-12% for transfer costs, property taxes, and fees. Developer payment plans can reduce initial capital requirement to 20-30%.

5. Where to invest in Islamabad real estate for best returns?

Highest appreciation potential (15-25% annually): CPEC route areas (currently undervalued), Mumtaz City and surrounding developments, new CDA sectors (E-12, D-12), commercial plots along emerging corridors. Best rental yields (6-8%): G-11, G-13 residential sectors, Bahria Town apartments, commercial shops in operational malls, areas near universities and hospitals. Balanced returns (income + growth): Mixed-use developments (Icon VIII, 5 West), DHA Islamabad (phases 1-2), F-sectors developed areas (F-10, F-11).

6. What is the average ROI on property investment in Islamabad?

Realistic annual ROI by property type: Residential apartments (ready): 12-18% (4-6% rental yield + 8-12% appreciation), Commercial properties: 13-20% (7-10% rental yield + 6-10% appreciation), Residential plots: 10-15% (pure appreciation, no rental income), Mixed-use developments: 18-28% (higher rental yields + strong appreciation), Emerging area plots: 15-25% (pure appreciation with higher risk). Total returns include both rental income and capital appreciation. Always calculate net rental yield after deducting maintenance, vacancy, and property tax (typically reduces gross yield by 1-2%).

7. How long does it take to complete a property purchase in Islamabad?

Timeline varies by property type: Ready possession properties: 6-12 weeks (research to ownership), Under construction: 1-4 years depending on project phase, Plots with possession: 6-10 weeks, Plots in developing societies: 1-3 years until development completes. Breakdown for ready properties: Research and property selection (1-2 weeks), Verification and due diligence (1-2 weeks), Negotiation and agreement (1 week), Payment and transfer (2-3 weeks), Post-purchase setup (1-2 weeks). Delays often occur due to incomplete legal documentation (+2-8 weeks), title disputes (avoid these), or outstanding dues (+2-4 weeks).

8. What are the hidden costs of buying property in Islamabad?

Beyond the property price, expect these costs (typically 8-12% of purchase price): Mandatory costs: Stamp duty (2-3% of property value), Registration fee (~1%), Capital Value Tax (CVT): 2% (for filers), 5% (non-filers), Transfer fee (variable by society), Legal verification (PKR 20,000-50,000), Documentation (PKR 15,000-30,000). Optional but recommended: Property inspection (PKR 10,000-25,000), Professional negotiator (1-2% of savings), Property insurance (0.1-0.3% annually). Post-purchase: Minor repairs/renovation (PKR 50,000-2 lakh), Furnishing if renting (PKR 1-3 lakh), Utility transfers (PKR 10,000-20,000).

9. Should I buy under-construction or ready property?

Choose under-construction if: You can wait 2-4 years for possession, Pre-launch discount exceeds 20%, Developer has excellent track record, You don’t need rental income immediately, Location has exceptional growth potential. Choose ready possession if: You need immediate rental income, Investment timeline is shorter (3-5 years), You want lower risk, You prefer to see finished product before buying, You value liquidity (ready properties sell faster). Data shows: Ready possession generates 3-5% higher annual returns when factoring in immediate rental income, despite potentially higher purchase price. Under-construction only outperforms with significant launch discounts (20%+) and exceptional location.

10. How do I verify a property is legally clear in Islamabad?

Complete verification checklist: Title Verification: Verify ownership at land records office (Patwari), Check 30-year ownership chain, Confirm no mortgages, liens, or disputes, Validate inheritance documents if applicable. NOC Verification: Confirm CDA/Development Authority NOC (check online via CDA portal), Verify building plan approval (for constructed properties), Check completion certificate (for finished buildings), Validate society’s legal status. Physical Verification: Survey measurements match documents, Plot marked correctly with corner pillars, No encroachments by neighbors, Built structure matches approved plans. Financial Verification: All utility bills cleared, Property tax paid to date, Development charges cleared, No outstanding dues. Cost: Professional verification costs PKR 30,000-60,000 but prevents losses of lakhs. M Realtors provides complete verification reports within 7 days.

Your Investment Journey Starts Here

Property investment Islamabad 2026 offers one of the most compelling risk-reward profiles in Pakistan’s economy. With stable appreciation averaging 12-18% annually, rental yields of 4-7%, and a transparent regulatory framework, Islamabad stands apart as the smart investor’s choice.

But success requires more than capital—it demands market knowledge, thorough due diligence, strategic planning, and often, professional guidance to navigate the complexities of real estate investment.

Whether you’re a first-time investor taking your first step into real estate, an overseas Pakistani investor building wealth back home, or an experienced portfolio builder diversifying assets, the insights in this guide provide the foundation for making informed decisions.

Remember: The best time to invest in Islamabad real estate was five years ago. The second-best time is today—before the next infrastructure project, the next society development, the next price appreciation cycle puts your target property out of reach.

Your next move:

Don’t let analysis paralysis prevent you from building wealth through smart investment. Schedule a no-obligation consultation with M Realtors today. Let’s discuss your goals, evaluate investment options, and create a property investment strategy designed specifically for you.

The property that will transform your financial future is waiting. Let’s find it together.

Contact M Realtors for Free Investment Consultation

Because smart investment isn’t about spending money—it’s about making money work for you.

Add a comment